More on the turn from zero budgets

29/01/2013 § 5 Comments

My last post said that it was good to see the Government thinking my way. Specifically, its economic policy depended on a coupled austerity-Christchurch rebuild plan that didn’t work out. They have, I believe, seen the light on Christchurch and are turning away from austerity, i.e., zero budgets.

Eric Crampton of Offsetting Behaviour commented. My reply got too long so here it is, with pictures.

Eric’s comment was:

RBNZ moves last, though, right? And we’re nowhere near zero bound. Why go for fiscal pushes that might have RBNZ more reluctant to drop rates or might have ‘em increase rates more quickly?

Or are you taking recent inflation #s as saying that RBNZ is targeting a medium term that’s farther away than you’d want?

So, first, yes, RBNZ moves last. If the Government looks like it is going to overheat the economy with fiscal policy then the RBNZ will move to counter it. That doesn’t mean I subscribe to monetary fatalism, the idea that we can’t do anything with fiscal policy because the central bank will shut us down. This applies forward and backward. I don’t agree that we couldn’t have done any better because the Bank wouldn’t have let us.

Note, of course, that the RBNZ may have had the right perception or the wrong one of the impact of Government spending. It is pretty clear from its Monetary Policy Statement of December 2012 (pdf) that they have been consistently optimistic:

However, the core of my comments is different. First, I could see the logic in the plan. Austerity for reasons of national economic policy — reducing the debt, placating overseas money markets — while getting some Keynesian intervention through Christchurch. Secondly, it didn’t work. It became clear in 2011 that it wasn’t working. Nevertheless, the Government stuck with the plan longer than I think they should have, and longer than the state of the economy warranted.

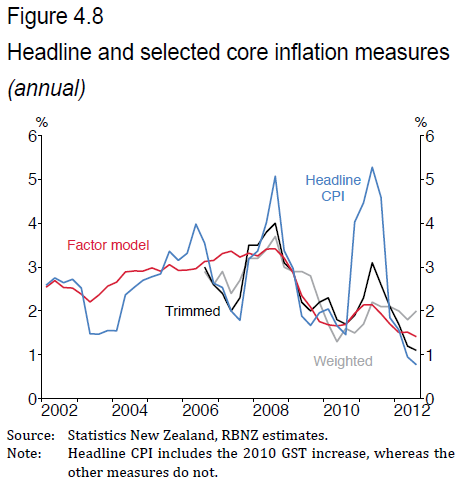

But, Inflation! I hear you cry. Well, yes, but:

The headline inflation numbers certainly suggest that the RBNZ needed to be careful in 2011, and that there wasn’t room for more Government spending. The other measures of inflation, however, suggest that the spike shouldn’t have driven policy, that core inflation barely breached the 3% top of the band, and it was falling towards the low end of the band through the second half of 2011 and all of 2012. So, inflation anxiety probably shouldn’t have driven policy.

The other graphs tell what I think the real story of the economy has been over the last 18 months. Unemployment up and not falling:

…and a pretty anemic recovery by historical standards:

For two years I’ve been telling cabbies and barbers and anyone else who asks, we are moving sideways and will continue to move sideways until someone actually does something different. So, once again with less bravado: Yay! Good to see some public investment in the economy when there is spare capacity and not much prospect of it being used anytime soon.

“Note, of course, that the RBNZ may have had the right perception or the wrong one of the impact of Government spending. It is pretty clear from its Monetary Policy Statement of December 2012 (pdf) that they have been consistently optimistic”

This all comes back to the RBNZ though – in so far as the slow recovery was due to “insufficient” demand, this is the responsibility of the central bank, not fiscal policy.

Now you come up with the excuse for them – the delays to the rebuild, which they could not foresee, led them to leave monetary conditions tighter than was warranted. The central banks reaction function was based on an assumption that didn’t come to light. This is consistent with the data which suggests:

1) Inflation was low,

2) Unemployment was elevated,

3) NGDP plummeted.

Unless we are explicitly saying that we expect the RBNZ to fail going forward, government policy can still be judged primarily on supply-side grounds. As a result, infrastructure policy et al can still be judged in a standard rate of return, there is no need to appeal to cyclical arguments.

I’d note that I support countercyclical infrastructure investment and deficits as a matter of course – and I’m not disagreeing that infrastructure spending could have been objectively too low. Just if we make a cyclical “macro demand” argument, we need to assume central bank failure before we can start talking about the relevance of fiscal policy.

Oww, sidenote – I don’t think the RBNZ would fail, and would never premise anything on that. I just wanted to make it clear that this is the assumption that would be needed.

They know what they are doing, they just work in a tough uncertain world, and in that environment we won’t get policy that looks “ex-post perfect”.

[…] Kaye-Blake notes the macroeconomic consequences of the delayed Christchurch rebuild, and wonders whether we consequently should have more stimulatory monetary policy: First, I could […]

[…] the RBNZ has been consistently optimistic about the economy over the last several quarters, predicting increases in the OCR that didn’t eventuate. As part of that, the Christchurch […]

[…] Kaye-Blake notes the macroeconomic consequences of the delayed Christchurch rebuild, and wonders whether we consequently should have more stimulatory monetary policy: First, I could […]